Facebook’s nudge towards digital currency is generating a tsunami of commentary and hand-wringing. Banks are right to be apprehensive, as very large, capital-rich tech giants who already have a relationship with their clients are now eyeing up their markets. To adapt, financial services have to accelerate their planning for a world where value exchange happens over open Web protocols.

In this article I discuss what Facebook-backed Diem (formerly known as Libra), digital currency is, how it fits into the broader picture of technological disruption facing incumbent banks, and what banks can do to counter these threats.

Contents

- What is Diem?

- How is Facebook involved, and why is this important?

- Short-term impacts

- Longer-term impacts

- What are the risks to banks?

- What should banks do?

What is Diem?

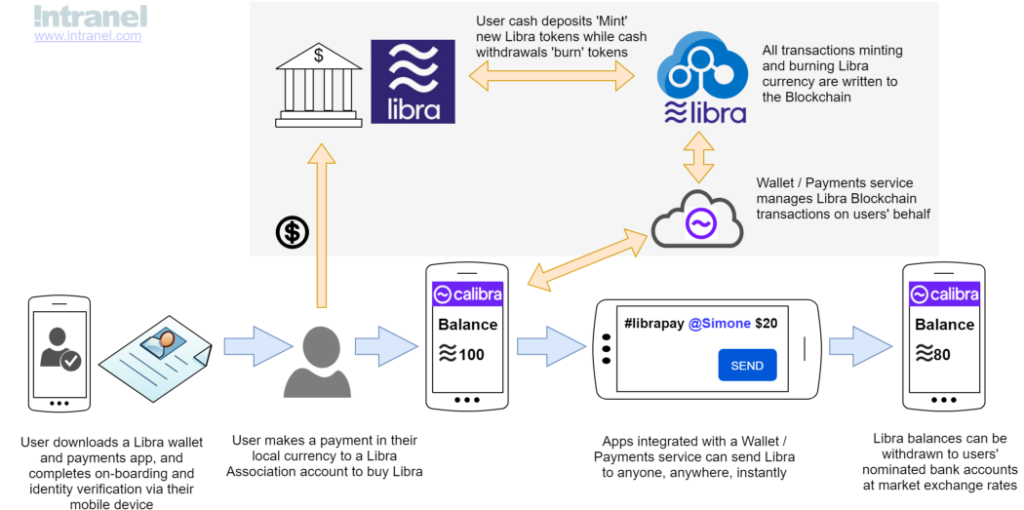

Diem is a new crypto-currency protocol. As such, it enables tokens representing the value to be transferred safely via the Internet. It also supports smart contracts so that the rules for how tokens are transferred can be defined in code for a given situation—essentially “programmable money”.

Diem is an asset-backed stable-coin, so its value will remain stable relative to major global currencies. It’s designed to be a global currency from day one. Diem is not a decentralised protocol like Bitcoin; users will need to trust the Diem Association (formerly known as Libra Association) to maintain the assets like bank deposits backing the tokens in circulation.

This centralisation also means that the currency and its users will need to comply with financial services regulations in their jurisdiction—(pseudo) anonymous transactions won’t be supported. As such, it really can’t be lumped in the same basket as most cryptocurrencies, and criticisms about lack of traceability and calls for a halt to implementation plans (whatever that means) are not justified at this stage of development.

It is likely that initial Diem applications will focus on payments, including peer-to-peer transactions and overseas remittances. The remittance payments aspect has the laudable aim of helping the world’s 1.7 billion unbanked people (most of whom have mobile devices) avoid the current extortionate fees they pay to transfer funds.

How is Facebook involved, and why is this important?

Facebook is a founding member of the Diem Association, the governance consortium set up to develop the Diem protocol, manage network nodes, and hold the assets backing the Diem token’s value.

The Diem distributed governance model combined with an open-protocol Blockchain-based approach is partly designed to alleviate some of the trust issues Facebook would face if they were to act in isolation. It’s worth noting that any other social network or platform (including banks) can integrate with Diem in the same way as Facebook.

Facebook’s involvement is hugely significant as they have a massive user base and no vested interest in maintaining the status quo for financial services. Diem integrations with Facebook, Messenger, WhatsApp, or Instagram would immediately expose those services to billions of users. Facebook may be aiming to emulate the payments market dominance of Alipay and WeChat in China. WeChat, in particular, has grown from a social media app to become China’s “app for everything”, and is considered a credible threat to Visa and Mastercard.

Facebook is also creating a subsidiary, Novi (formerly known as Calibra) which will be Facebook’s digital wallet for storing Diem coins, available initially in WhatsApp and Messenger. Novi is very much Facebook’s own play, and only transfers outside the Novi system will be written to the Diem Blockchain. This approach will enable Novi-based Diem transactions to scale to the size of the Facebook user base, something that would be technically challenging with a blockchain-only approach.

Facebook’s involvement has attracted other major players to the Diem association, including nominal competitors such as Visa and Mastercard. These organisations are hedging their bets for a (relatively) small upfront investment of ~$15m USD. There is a perception among the Blockchain community that if Facebook moves aggressively with crypto technologies, FOMO will kick in and other major organisations will be forced to follow. The idea that Blockchain tech is going mainstream has been partly responsible for recent rapid rises in the price of cryptocurrencies such as Bitcoin.

Short-term impacts

Technically, Diem is still behind many existing stablecoin projects, with a target launch date “sometime in 2022”. Despite being described as a full-frontal assault on the payments industry the limited level of resources going into the venture (especially given the many tech and compliance hurdles to overcome) indicate it’s not yet cored to Facebook’s strategy.

Short-term, the biggest impact is probably raised awareness of the potential impact of Distributed Ledger Technologies in financial services, and a change in the competitive landscape—Diem is motivating financial services to accelerate their strategy to plan for a world where most value exchange happens over open Web protocols— a democratisation of FinTech.

Medium-term, expect Diem to take a significant slice of the overseas remittances market. If good on-ramps and off-ramps between Diem and local currencies are developed in target countries this will impact existing transfer services and the use of (more volatile) Bitcoin for this purpose.

Support for on-ramps and off-ramps with local currencies requires connections with conventional banks and local partnerships on the ground. As banks well know, compliance processes and partnerships across multiple jurisdictions take time and effort to build. For developing countries there is some risk a new global currency with excellent device connectivity may usurp the local currency and impact central banks’ ability to regulate the money supply, leading to regulatory push-back. As Diem is backed by “a basket of bank deposits and short-term government securities” it may also be considered a security, with significant regulatory and tax implications. As such, it’s unlikely Diem services will scale massively in a short time frame.

Financial services, and increasingly even crypto-currencies already have well-established rules (relative to social media) and this relative clarity may make Facebook’s job easier. They can focus on friendly geographies with responsive regulators first, and build acceptance from there.

- A Diem based network running on mobile devices could offer retailers an alternative to Point-of-Sale (POS) networks and credit cards, creating downwards pressure on the fees merchants will pay for accepting payments.

- Support for local currencies is possible via some sort of automated hedging arrangement with Diem. Consumers feel more comfortable dealing in local currency so this will be necessary for traction in many local payments markets.

- Diem may prompt a shift of peer-to-peer payments away from bank transfers to social media channels by offering a better user experience

- It could become a standard for online micro-payments, with positive impacts on content providers — imagine a “like-plus” button that instantly donates $0.25 for an excellent piece of journalism.

Don’t expect the payments ecosystem to be disrupted overnight. Credit card use is entrenched with rewards programmes and free credit, and POS networks already offer relatively low-cost transactions, so it’s not an immediate existential crisis for these providers.

Cross-border payments and online shopping tend to attract higher credit card fees and cost merchants more in fraudulent (reversed) transactions and this is an area where merchants would be more likely to encourage use of Diem and pass on savings to consumers.

Longer-term impacts

The financial services market has already seen significant fragmentation due to new technologies and changing regulatory landscapes.

Diem and similar protocols may herald a paradigm shift in how financial services are delivered. Once money becomes programmable and its flow can be controlled with negligible friction via open protocols, then barriers to entry for all forms of financial products are reduced.

Globalised, programmable money enables the building of globalised securities markets, insurance products, and other financial services while reducing the need for local bricks and mortar. The use of Blockchain-based records, digital identity and mobile biometrics, and dis-intermediation of gatekeepers between consumers and services will enable higher levels of automation and may actually make it easier for regulators and citizens to manage compliance and tax obligations.

Banks will no longer be sitting in the middle of most financial services so fewer consumers will default to using their bank for all their financial needs. Future customers will no longer need a relationship with a traditional bank and will pick and choose services from a larger variety of offerings.

Central bank issuance of tokenised fiat currency may give governments more flexibility around money creation and impact the privileged position of banks. Several central banks are investigating options for tokenised (programmable) fiat currency.

International regulations will need to adapt to new technologies but countries won’t want to be shut out of the potential up-side. Regulation may slow the process but is unlikely to stifle it — many countries and trading blocks like the EU are already well aligned on financial regulation.

What are the risks to banks?

The Diem project signals that very large, capital-rich tech giants who already have a relationship with most existing bank customers are eyeing up profitable financial services markets.

It would be an overstatement to say Facebook’s Diem move changes everything overnight. However, a combination of technological and social trends towards automation and online delivery of services means that tech giants (or those banks that adapt) are well-positioned to take large chunks of the global financial services market.

Banks’ payment services could be left by the wayside, just like personal navigation devices were by Google Maps, if they don’t adapt. If banks lose market share around transactional banking then consumers (especially digital natives) will be likely to shift future lending business to those new relationships (even more so if lower interest rates are on offer via more efficient service delivery).

The tech giant businesses—Facebook, Apple, Amazon, Netflix, and Google (FAANG)—are a unique class of competitors because they:

- Think on a global scale

- Already deliver online services at a massive scale

- Know how to manage Big Data and utilise Machine Learning

- Can build market share with loss-leading services

- Don’t have the legacy infrastructure or a vested interest in maintaining the status quo—they may well be happy to open financial ecosystems to all and sundry, especially if it mitigates antitrust risks

Banks, on the other hand, have market share and deep sector knowledge but are saddled with legacy infrastructure, which combined with a risk-averse culture makes genuine innovation difficult.

While forays to date have mostly been in partnership with incumbents (for instance, Apple Pay largely sits on top of existing payments infrastructure), Diem (or similar technology) has the potential to sidestep existing providers.

On the other side of the ledger, an organisation like Facebook doesn’t have deep knowledge of financial services or a great track record dealing with the minutiae of local compliance. These skills can, however, be paid for, which means FAANG businesses pose a threat to core banking services.

Consumer and business lending is generally the core revenue source for retail banks, and the key to this is the evaluation of the creditworthiness of a potential borrower and the setting of appropriate interest rates.

FAANG businesses have access to customer meta-data that (when combined with Machine Learning) may give them significant advantages in assessing risks and creditworthiness. They also have access to validation data around a person’s online interactions, making on-boarding and compliance costs potentially much lower, and reducing risk. Self-sovereign digital identity projects mitigate Big Brother issues and will streamline compliance and provide mobile transaction verification, reducing the need for face-to-face interactions and favouring online business models. Millennials have demonstrated an expectation that everything that can be done online, should be.

Typical barriers to entry for banking licences (e.g., minimal capital requirements) are relatively surmountable for FAANG businesses, and this means these new entrants can access the key competitive advantage of being able to operate a fractional reserve model.

This threat from tech giants is manifesting at the same time as the creation of new financial instruments and associated markets become faster and more globalised. Access barriers for trading in these markets (and Forex markets) will be lowered and automation increased, putting pressure on banks’ margins from these trading streams. Banks can also expect continuing pressure on bank fees and commission revenue from insurance and fund products.

What should banks do?

Beat Diem to market

The best thing banks can do in the short term is to remove the incentive for consumers to adopt new payment technology en masse. This requires delivering meaningful open banking ahead of competing technology. This shouldn’t really be that hard, given that work is already underway in multiple jurisdictions through bodies like Payments NZ.

To be clear, open banking (in the sense of payments) means an open, public protocol that allows consumers and merchants to connect any app to their bank account, with limits they control so that the app can autonomously and instantly send money from their bank account to any other account, with zero or low fees.

Doing this effectively may require building parallel systems that bypass constraints of legacy infrastructure (such as batched processing).

With a working open banking protocol, banks can get the jump on Diem by building a payments app that integrates with social media and bank accounts. There’s clearly a capability in the sector to extend existing apps like ANZ’s Pay-to-Mobile.

Get on top of new technologies

A strong capital position and sticky customer base remain a major advantage for banks. The trick is to exploit this to win the race with services that leverage new technologies while minimising the impact of a risk-averse culture. This usually means creating separate business units with new brands and real freedom to take risks.

Innovation hubs or “skunk works” should be funded sufficiently, with outputs that are intended to drive core business rather than being an afterthought to generate PR. Banks need to be prepared to let their innovation teams cannibalise their own revenue streams and impact long-standing business relationships—if they don’t someone else will. The risks are real but can be managed via many mechanisms including limited beta trials and good management of user expectations.

Leaders need to drive and incentivise change. Enabling people to risk doing new and better things also means giving them permission to fail. A starting point may be to reduce the number of people who can veto new ventures; anecdotally, we’ve heard of projects requiring 19 different sign-offs, many of whom have more incentive to say no than yes.

Banks can work with technologists and entrepreneurs with a track record of creating new products to help build efficient innovation processes. Alternatively, buy some FinTech companies with this culture and let them loose.

Focus on investment banking activities

Tech giants excel with processes that can easily be automated. Investment banking services, in particular, tend to be complex and dynamic and lend themselves to expert teams rather than (pure) automation. Advisory services, securities trading, managing mergers, acquisitions—they all require intensive (often local) knowledge and are not going to be low-hanging fruit for the competition from tech giants.

If you can’t beat ’em, join ‘em

There’s no reason why banks can’t integrate with the Diem protocol. Banks could make it super easy for customers to access Diem by providing direct off-ramps and on-ramps for local currency and include Diem wallets within new payments apps, reducing the need for customers to use Facebook’s proprietary Novi wallet.

There is also an opportunity for banks to join the Diem consortium, gain deeper insights into the changing landscape, and help shape the future.

Over time partnering with tech giants may make sense—this could mean offering compliance and credit risk assessment services locally and local physical points of presence.

Banks could do something really interesting and build some new services around Diem—how about a global secondary market for securities? There’s no fundamental reason why anyone, anywhere with Diem who has been properly on-boarded shouldn’t be able to go online and in 10 minutes acquire some tokens that provide all the risks and benefits of owning half an Apple share.

While banks may struggle to be as lean and efficient as new entrants building on protocols like Diem, they can work on identifying those businesses that are succeeding, with a view to either acquisition or building close partnerships.

Final thoughts

Everything the tech giants are missing to become the most efficient providers of consumer financial services they can buy. Banks on the other hand also have plenty of capital but may struggle to do the same thing because of cultural barriers to innovation.

Banks do have a proven ability to adapt when forced to, either through changing regulations or immediate competitive threats.

The bigger winners, in this case, will be those that move before they are forced to and divert some dividends to genuinely invest in delivering open banking and new services, ahead of new entrants to the market. Banks need to plan for a world where most value exchange happens over open Web protocols.

The trend towards online-centric business models will continue.

Banks must invest in automation and innovation, and be prepared to cannibalise their own revenue streams as well as becoming more lean in order to guarantee future market share. High street banking models will continue to become less sustainable in the face of online-focused competition and a new generation of ‘digital native’ consumers.

On the bright side, there are major opportunities as global currencies.

A connected world and aligned regulations mean new financial products can begin to access global markets while minimising local points of presence.

Just because banks have been highly profitable for many years doesn’t mean their business model can’t be disrupted. The eventual winners are planning and investing now for a landscape that may change more in the next 5 years than in the 20 before that.

Article by

Adam Lyness

Co-founder, Business Development Manager @ Intranel